Decoding TSMC: The Market Sees a Rocket Ship, I See a Stress Test

The pre-earnings ritual is in full swing. On October 16, Taiwan Semiconductor Manufacturing Co. will pull back the curtain on its third quarter, and the consensus on Wall Street feels almost uncomfortably uniform. Analysts are tripping over themselves to raise price targets. Susquehanna’s Mehdi Hosseini sees a “beat and raise” quarter, bumping his target to a cool $400. Barclays is right there with him. The narrative is set: AI is a tidal wave, and TSMC is the world’s only surfboard manufacturer.

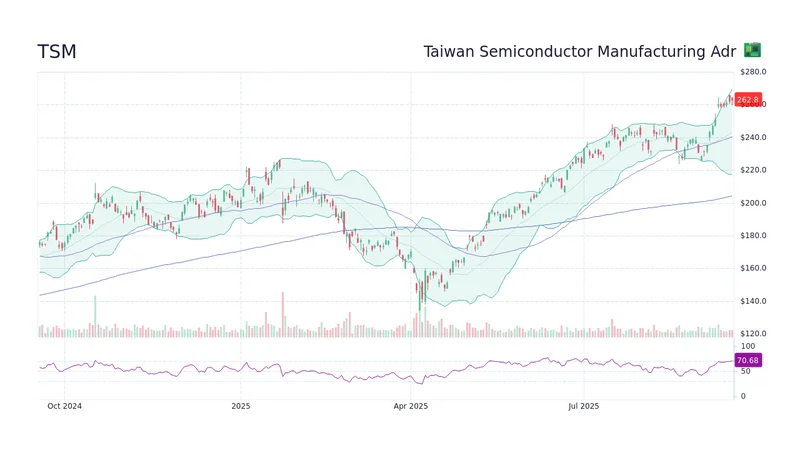

The headline numbers certainly feed this optimism. Wall Street expects earnings per share to jump more than 34% year-over-year to around $2.63. Revenue is projected to land near $32 billion—or $32.07 billion, to be more exact—a figure that aligns neatly with the company's own guidance. With year-to-date performance already up over 42%, handily outpacing the broader tech sector, it’s easy to get swept up in the momentum.

But I’ve looked at hundreds of these pre-earnings reports, and this particular setup feels… different. The market is pricing TSMC for perfection, treating it as a pure-play bet on the AI revolution. I see something else. I see a colossal, intricate machine being pushed to its absolute operational limits, and the first signs of strain are starting to show up in the data if you bother to look past the headline revenue figures. The real story isn't about the AI boom. It's about whether the company that powers that boom can withstand the pressure of its own success.

The Margin of Error

Let’s talk about the numbers that aren’t getting the same prime-time coverage. While TSMC’s September revenue was up an impressive 31.4% year-over-year, it actually edged down 1.4% from August. A minor dip, to be sure, but a deceleration nonetheless. More importantly, the company’s own guidance projects a gross profit margin between 55.5% and 57.5%. That’s a notable step down from the 58.6% it posted in the previous quarter. This isn't just a rounding error; it's a signal.

This margin compression is the crux of the matter. TSMC is the undisputed king of advanced semiconductor manufacturing. Its 3nm and 5nm nodes are the bedrock upon which companies like Apple, Nvidia, and AMD build their empires. This technological moat has always been its greatest strength, allowing for incredible pricing power. Think of TSMC as the only chef in the world who holds the secret recipe for the most in-demand dish. For years, they could name their price. But now, the chef is being forced to open new, incredibly expensive kitchens in Arizona, Japan, and Germany to satisfy that demand.

These new fabs are a geopolitical necessity, diversifying the company away from the ever-present risk of regional instability. But they come with a brutal price tag. Higher labor costs, higher energy costs, and the unavoidable inefficiencies of ramping up new facilities are projected to drag down gross margins by 2-3 percentage points annually for the next several years. This is the friction the market seems to be ignoring. The question is no longer just "how much can they sell?" but "how much will it cost them to sell it?" Is this margin pressure a temporary, manageable cost of doing business, or is it the beginning of a long-term erosion of the very foundation of TSMC's valuation?

And this is the part of the analysis that I find genuinely puzzling. While the street’s top analysts maintain a "Strong Buy" consensus, other quantitative models are flashing yellow. The Zacks model, for instance, does not predict an earnings beat, citing a negative Earnings ESP (Expected Surprise Prediction of -0.48%). This discrepancy between the qualitative, forward-looking analyst sentiment and the quantitative, backward-looking model is precisely the kind of divergence that warrants skepticism. It suggests the underlying data contains weaknesses that the prevailing narrative is glossing over, leaving investors to wonder, Should You Buy, Sell or Hold TSM Stock Before Q3 Earnings Release?

The recent 8% drop in the stock over five trading days, ostensibly linked to Trump’s tariff threats, is another piece of the puzzle. While many dismiss it as political noise, it reveals a deeper fragility in market sentiment. The stock is priced for flawless execution in a perfect geopolitical environment. When either of those assumptions is questioned, even hypothetically, the valuation gets shaky. How much of the company’s future growth is already priced in, and how much room is there for disappointment?

A Test of Foundational Strength

Ultimately, the bull case for TSMC is simple, powerful, and probably correct in the long run. The company is the central nervous system of the global technology ecosystem. AI is real, and the demand for high-performance computing isn't going anywhere. But investing isn't just about identifying a great company; it's about assessing its valuation against its near-term operational risks.

The upcoming earnings report on October 16 will be less of a referendum on the AI boom and more of a stress test on TSMC’s ability to manage its own sprawling, increasingly expensive global empire. Ignore the headline revenue beat that will likely come. Watch the gross margins. Listen to the guidance on capital expenditures and the operational costs of the new fabs. That's where the real story will be. The market is watching a rocket launch, but the most important metrics are the ones that tell us if the engine is overheating.