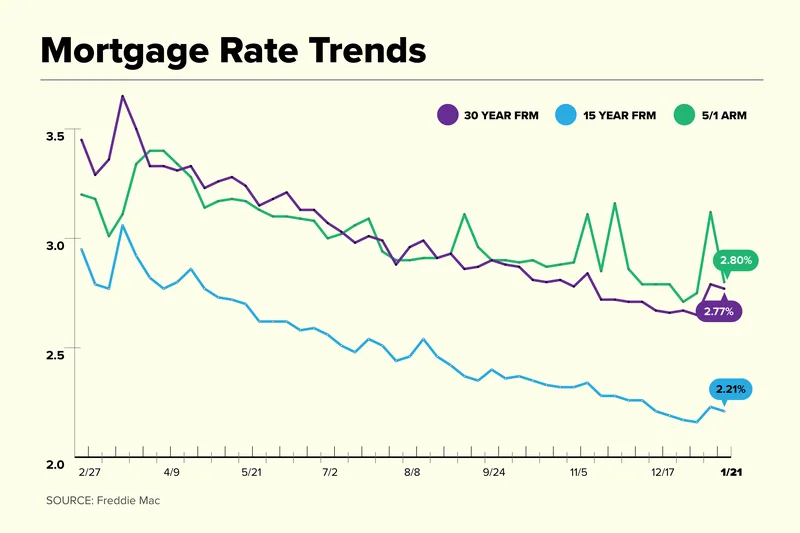

So, I’m staring at headlines like "Mortgage and refinance interest rates today, October 18, 2025: Rates hit their lowest point of 2025," and I’m supposed to be impressed. The 30-year fixed rate has graciously dipped to 6.18%. Break out the champagne, folks. We’re saved.

Give me a break.

Celebrating a 6.18% mortgage rate as a victory is like being grateful your captor loosened your chains by a single link. Sure, it’s technically better than the 7%+ nightmare we were staring down in January, but let’s not pretend this is some kind of consumer salvation. This isn't a win; it's just a slightly less painful loss. The entire narrative feels engineered to coax shell-shocked buyers back into a market that’s fundamentally broken.

The experts, in their infinite wisdom, are telling us that now "could be a good time to lock in a rate." Offcourse it is. It's always a good time to buy, according to the people who make money when you buy. It doesn't matter if you're signing up for three decades of payments that will bleed you dry—just get in the game! What they don't tell you is that the game is rigged.

The Golden Handcuffs and the Illusion of Choice

Let's be real about the state of play. The American housing market isn't a market anymore; it's a hostage situation. Anyone who was lucky or smart enough to refinance or buy when home mortgage interest rates were hovering around 3% during the pandemic is now shackled to their property with golden handcuffs. They can't move. Selling their home would mean trading a laughably cheap mortgage for one that's double the cost, for a house that's probably smaller and in a worse neighborhood.

So, who's left to buy? People like you and me, the ones who missed the boat. We’re being offered the "deal" of a 6.18% rate to buy inventory that's artificially scarce because no one with a good rate is selling. This whole situation is like a game of musical chairs where the music stopped three years ago. The people in the chairs are refusing to get up, and the real estate industry is just frantically trying to convince the rest of us that it's fun to stand around and watch.

Are we really supposed to feel good about this? Is the new American Dream just finding a house you can barely afford and then praying you never have to move again for the rest of your life? It feels less like building equity and more like entering a long-term financial prison. And don't even get me started on using a mortgage calculator these days. Punching in the numbers for a median-priced home at these rates is an exercise in pure masochism. You see that final interest payment and you just have to laugh, or you'll cry.

This whole mess reminds me of my dad trying to fix our old lawnmower. He'd spend hours tinkering, convinced that one more tweak would get it running smoothly. But the engine was shot. It didn't matter how much he adjusted the carburetor; the fundamental problem remained. That's the housing market. The Fed, the lenders, the economists—they're all tinkering with the rates, but the engine of affordability is completely seized.

Don't Thank the Fed for This "Relief"

Now, let's talk about the Federal Reserve, the supposed puppet master of our financial lives. Everyone is breathlessly waiting for the next round of Fed rate cuts mortgage interest rates are supposed to follow, right? Wrong. This is the biggest shell game of them all.

The Fed cuts its little short-term rate, and the headlines blare. But your 30-year mortgage rate barely budges. Why? Because mortgage rates don't actually follow the Fed. No, they're tied to the 10-year Treasury yield, which is a fancy way of saying they're tied to what big-shot investors think about the economy's health over the next decade. And right now, those investors are still spooked by inflation and government debt.

What's even more insulting is that by the time the Fed actually announces a cut, the market has already "priced it in." Lenders have already adjusted their numbers in anticipation. So the big announcement day comes and goes, and for the average person looking to refinance mortgage debt or buy a home, absolutely nothing changes. It's all just theater. This is a bad idea. No, "bad" doesn't cover it—this is a deliberately confusing system designed to benefit the institutions, not the individual.

So when you see headlines that mortgage interest rates drop, you have to ask: for who, and for how long? We saw rates dip right before the Fed's September meeting, only to spike again weeks later. It's a volatile, unpredictable mess. Trying to time this market is a fool's errand. It ain't a strategy; it's gambling with the biggest purchase of your life. And the house always wins.

The advice to "improve your credit score" and "shop around" feels so hollow right now. It's like telling someone drowning in the ocean to try swimming a little harder. Yes, it's technically good advice, but it completely ignores the hurricane-force winds of a broken system. Then again, maybe I'm the crazy one for thinking a system this big could ever be designed for the little guy...

So We're Just Supposed to Get Used to This?

Look, I get it. The days of 2.65% are a historical anomaly, a fever dream we'll tell our grandkids about. But this collective shrug as we settle into a "new normal" of 6% rates is infuriating. This isn't normal; it's a massive downward revision of financial possibility for an entire generation. We're being told to accept less, pay more, and be grateful for the privilege. Don't fall for it. This "lowest rate of the year" isn't a gift. It's a breadcrumb, and we should be demanding the whole loaf.