A 4.1% single-day jump in a stock is always worth a look. For PayPal (PYPL), a company whose stock chart over the last few years resembles a painful downhill slope, any green day feels like an event. The catalyst this time was the announcement of PayPal Ads Manager, a new platform designed to let its millions of small business clients monetize their own traffic. The market, ever hungry for a new narrative, nibbled. The stock popped. The move was captured in headlines like PayPal stock climbs after launching ad platform for small businesses (PYPL:NASDAQ).

On the surface, the logic is sound. PayPal sits on a treasure trove of transactional data, arguably one of the most valuable datasets on consumer behavior in the world. Leveraging this to create an advertising network seems like a natural, almost overdue, extension of its business model. The plan allows merchants to generate ad revenue with no upfront cost, a compelling proposition for the small businesses that form PayPal's backbone. The service is slated for a US launch in early 2026.

But a single-day rally—one that didn't even hold its full gains by the close, settling at a 3.6% increase—is just noise. It’s a flicker of sentiment. The real work is to place that noise in the context of the much louder, more persistent signal the market has been sending about PayPal for years. And that signal is one of deep, structural concern. Is a new ad platform, one that won't even generate revenue for over a year, enough to change the fundamental equation? Or is this just a fresh coat of paint on a creaking edifice?

A Pop in a Vacuum

Let's first deconstruct the market's brief enthusiasm. A 4% move isn't exactly earth-shattering for a stock as volatile as PayPal, which has seen 11 moves greater than 5% in the last year alone. In that context, the market’s reaction reads less like a fundamental re-evaluation and more like a sigh of relief that the company is, at least, trying something new. Analysts have pointed to advertising as a potential growth vector for a while, so the announcement serves as a confirmation of a long-held thesis. It’s a predictable move, not an innovative one.

The platform itself is a classic data-play. By analyzing its vast repository of payment information, PayPal can theoretically help brands place highly targeted ads on its merchant network. Think of it as turning every small online store using PayPal into a tiny, specialized billboard. It’s an elegant concept, a closed-loop system where commerce and advertising feed each other. It also comes on the heels of another announcement: a partnership with India's UPI system to streamline international payments. On paper, these are positive developments.

And this is the part of the report that I find genuinely puzzling. The market reacted to a press release about a future product. There are no revenue projections, no margin estimates, no early adoption metrics. We are, in essence, capitalizing a concept. What is the projected revenue contribution of this new venture in, say, 2027? And more critically, what is the expected margin on that revenue? Without those figures, we're just trading on a story. It feels like a ship captain, whose vessel is taking on water, proudly announcing that a new espresso machine will be installed in the galley next year. It’s a nice feature, but does it address the primary problem?

The announcement also conveniently landed just a week after the stock dropped 3.8% on news that OpenAI was deepening its relationship with Stripe, a key competitor. That partnership allows users to buy physical goods, a direct incursion into PayPal’s territory, powered by a more nimble and developer-friendly rival. This competitive pressure is the leaky hull, and I’m not yet convinced an ad platform is the right tool to patch it.

The Crushing Gravity of the Long-Term Chart

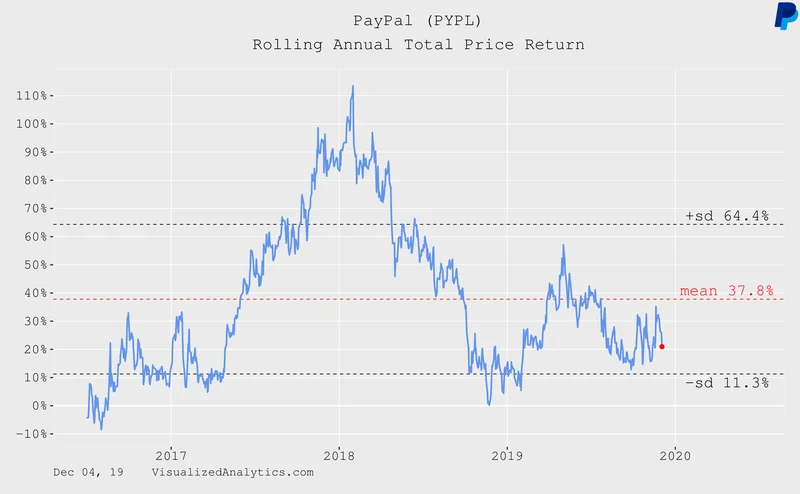

Now, let's zoom out from the single-day chart and look at the bigger picture. The numbers here are clinical and brutal. PayPal's stock is down about 14% this year—to be more exact, 14.3% since the beginning of 2025. It’s trading nearly 20% below its 52-week high.

But the truly staggering figure is the five-year return. An investment of $1,000 in PayPal five years ago would now be worth $379.61. That’s a 62% destruction of capital. This isn't a dip; it's a collapse. It represents a fundamental loss of faith from long-term investors, a belief that the company's competitive moat has been irrevocably breached by the likes of Stripe, Apple Pay, and a host of other fintech innovators.

Against that backdrop, a 4.1% pop on a pre-revenue product announcement looks less like the beginning of a turnaround and more like a dead cat bounce. It's a momentary spasm of hope in a long, downward trend. The market is desperate for any sign that PayPal's management has a credible plan to restore growth and fend off the competition that is relentlessly eating away at its core business.

The core problem for PayPal isn't a lack of adjacent revenue streams. The problem is that its primary value proposition—being the default, easy-to-use digital wallet—is no longer unique. Competition is fierce, and innovation from rivals is rapid. OpenAI choosing Stripe isn't just a lost contract; it's a signal of where the next generation of digital commerce is heading. Is PayPal positioned to win that future, or is it trying to monetize its past? This new ad platform feels like an attempt to wring more value from its existing user base, a defensive move, rather than an offensive one to capture new ground.

A Tactical Band-Aid on a Strategic Wound

Ultimately, the launch of PayPal Ads Manager is a logical, if uninspired, move. It's a sensible way to leverage a core asset—its data. But it is not a silver bullet. The market’s fleeting excitement is a distraction from the punishing arithmetic of the company's long-term performance and the intensifying competitive landscape. This isn't the strategic overhaul the company needs; it's a tactical addition that may, at best, add a few percentage points to the top line in a few years' time (assuming successful execution). The fundamental question remains unanswered: can PayPal's core payments business regain its momentum and fend off leaner, more innovative rivals? Until we see evidence of that, this ad platform is just a decimal point in a sea of red ink.