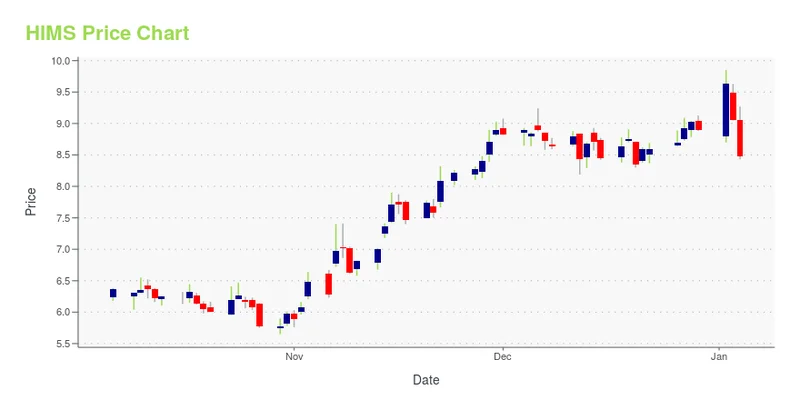

So, Hims & Hers stock is up 39% in a month. Let’s all just take a deep breath for a second and ask ourselves if we’ve collectively lost our minds.

We’re talking about a company that’s mastered the art of Instagram ads for hair loss and erectile dysfunction pills. And for that, Wall Street has apparently decided it’s the next big thing, a rocket ship to the moon. The `hims stock price` is screaming, the `hims stock news` is all breathless hype, and I’m sitting here wondering if I’m the only one who sees the emperor is wearing nothing but a well-branded, minimalist-packaged jockstrap.

This isn't investing anymore. This is fandom. It’s the same energy that pumps up `sofi stock` every time they run a Super Bowl ad or sends `tsla stock` to the stratosphere because of a cryptic tweet. People aren't buying a business; they're buying a story. And Hims is selling one hell of a story.

The Fairy Tale They're Selling You

You’ve got to hand it to them. The "narrative" is a masterpiece of Silicon Valley buzzword bingo. They’re not just a company; they’re a platform. They’re not just selling drugs; they’re "vertically integrating diagnosis, fulfilment, treatment, and retention." They’re not just a cash-only business; they’re "avoiding insurance entirely and personalising care at scale."

Give me a break.

This whole thing feels like a movie pitch. The hero (Hims) is bravely disrupting the big, evil dragon (the American healthcare system) by… selling generic drugs online without the hassle of a doctor's office. It’s a great pitch! It’s convenient! But is it a revolution worth a Price-to-Earnings ratio that makes your eyes water? One recent analysis, Evaluating Hims & Hers Health (HIMS) Valuation After 39% Share Price Surge in the Past Month, suggests the stock is still 32.8% undervalued, with a "fair value" of over $86. This valuation is based on what the source calls "extraordinary expansion plans" and "bold assumptions."

"Bold assumptions" is just corporate-speak for "we're pulling numbers out of thin air and hoping you don't notice." What are these financial moonshots, exactly? How does a company selling finasteride and sildenafil create a moat so deep that it justifies these numbers? Are we supposed to believe their branding is so powerful that no one else can set up a slick website and partner with a mail-order pharmacy? Because that model ain't exactly a state secret.

This is a marketing company. A damn good one, I’ll admit. Their ads are everywhere, their branding is clean, and they’ve successfully destigmatized conditions that people used to be embarrassed about. Kudos. But a great marketing department doesn’t magically transform a simple e-commerce business into the next `nvidia stock`.

A Cold Shower of Numbers

Now let’s get out of the fantasy world and look at the ugly numbers. While one group of analysts is writing fan fiction about Hims’ glorious future, another, more sober analysis asks the question, OMCL or HIMS: Which Is the Better Value Stock Right Now?, and ultimately slaps the stock with a “D” grade for Value from Zacks. A "D"! In school, that means you’re one step away from failing.

This valuation is insane. No, 'insane' is too kind—it's a collective delusion. Hims has a forward P/E ratio of 94.83. The industry average is around 21. For comparison, a competitor, Omnicell, has a forward P/E of 20.30 and gets an "A" for value. So you’re paying nearly five times the multiple for a company with weaker fundamentals, just because it has better branding and a story that appeals to millennials.

It’s completely disconnected from reality. It reminds me of all the tech darlings that call themselves "platforms." My cable company calls its glitchy on-demand menu a "content delivery platform." It’s a meaningless term used to slap a tech multiple on a non-tech business. Hims is a direct-to-consumer brand, full stop. A good one, but a simple one.

The market is rewarding Hims for its growth, offcourse. But what happens when that growth slows? What happens when the novelty wears off, or when Amazon inevitably decides to crush them by offering the same service for a few bucks less a month? What is the actual, durable advantage here? The slick packaging? I just don’t see it. They're selling a story of disruption, but at the end of the day...

This isn't a long-term plan for a sustainable business. It's a mad dash for customer acquisition fueled by venture capital logic, and now the public markets have to hold the bag. Then again, maybe I'm the crazy one. Maybe a telehealth company for lifestyle drugs really is the key to fixing American healthcare.

Yeah, and maybe I’ll win the lottery tomorrow.

This Is Just a Meme Stock in a Lab Coat

Let's be real. Hims isn't a healthcare company in the way UnitedHealth or even a hospital is. It’s a consumer brand that found a clever regulatory loophole to sell prescription meds like they’re subscription boxes for fancy coffee. The current `hims stock price` reflects a belief that this model is infinitely scalable and defensible, which is a laughable assumption. The moment a bigger player with deeper pockets decides this market is worth taking, Hims' high margins and growth narrative could evaporate overnight. People are buying the hype, not the balance sheet, and that’s a game that never, ever ends well for the little guy. Don’t get mesmerized by the 39% jump; look at the foundation it's built on. It's sand.

Stock: A Sober Look at the Price and Recent News")